Estimation of multivariate generalized gamma convolutions through Laguerre expansions

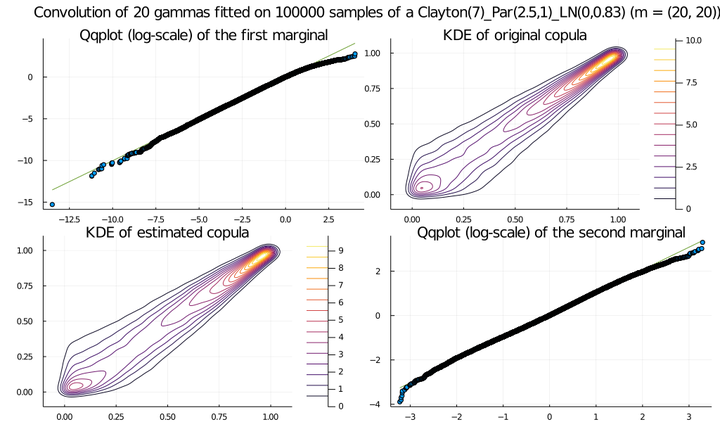

An exemple graph from the paper

An exemple graph from the paper

Abstract

The generalized gamma convolutions class of distributions appeared in Thorin’s work while looking for the infinite divisibility of the log-Normal and Pareto distributions. Although these distributions have been extensively studied in the univariate case, the multivariate case and the dependence structures that can arise from it have received little interest in the literature. Furthermore, only one projection procedure for the univariate case was recently constructed, and no estimation procedures are available. By expanding the densities of multivariate generalized gamma convolutions into a tensorized Laguerre basis, we bridge the gap and provide performant estimation procedures for both the univariate and multivariate cases. We provide some insights about performance of these procedures, and a convergent series for the density of multivariate gamma convolutions, which is shown to be more stable than Moschopoulos’s and Mathai’s univariate series. We furthermore discuss some examples.

Oskar Laverny

Maître de Conférence

What would be the dependence structure between quality of code and quantity of coffee ?